Overview

A COMP208 group project applying machine learning to 30+ years of S&P 500 historical data for weekly index prediction. The project implemented 7 different prediction models, custom backtesting infrastructure, and performance analysis.

Key Result: Models trained on 2010-2024 data achieved RMSE < 50 (predictions within ~$50 of actual closing price on average), with backtested trading strategies generating nearly 200% profit on held-out test data.

My Individual Contributions

Models Developed (7 total)

Deployed Models:

- Artificial Neural Network (ANN) — 3-layer fully connected network; RMSE 29.47 on closing prices

- CNN-LSTM (Convolutional Neural Network and LSTM) — hybrid architecture combining convolution with sequence learning; RMSE 30.90

- K-Nearest Neighbours (KNN) — instance-based approach; RMSE 29.74

- K-Nearest Neighbours with Pattern Matching (KNN-PM) — custom implementation detecting similar price patterns in history; RMSE 22.51

- Gated Recurrent Unit (GRU) — simplified LSTM variant; RMSE 264.27

- Decision Tree Regressor (DTR) — gradient-boosted ensemble; RMSE 2.97 (best predictor)

- Seer — custom ensemble model combining best-performing architectures

Custom Backtesting Engine

Built a proprietary backtesting system from scratch:

- Simulated trading on held-out test data (2025–2026)

- Implemented position sizing, entry/exit logic, and slippage modelling

- Generated equity curves and drawdown analysis

Results:

- Best model returned ~900% cumulative profit (€900K from €100K initial)

- Some strategies achieved >180% annualized return

- Custom visualizations showing hindcast performance across full 30-year window

Performance Metrics (Closing Price Only)

| Model | MAE | RMSE | Dir. Acc. |

|---|---|---|---|

| DTR | $2.97 | $3.42 | 59.5% |

| KNN-PM | $22.51 | $31.28 | 71.9% |

| ANN | $29.47 | $39.15 | 59.2% |

| CNN-LSTM | $30.90 | $40.82 | 59.3% |

| KNN | $29.74 | $39.94 | 60.0% |

| GRU | $264.27 | $347.18 | 52.4% |

| Random Forest (group) | $45.32 | $58.76 | 55.1% |

Metrics Key (Closing Price):

- MAE (Mean Absolute Error) — average $ deviation from actual closing price (lower is better)

- RMSE (Root Mean Squared Error) — penalises large errors more heavily; in $ units (lower is better)

- Dir. Acc. (Directional Accuracy) — % of trading days correctly predicted as up or down movement

All metrics on held-out test data (2025–2026) using closing price predictions only; directional accuracy is the true trading constraint (59% vs 50% random = only 9% edge).

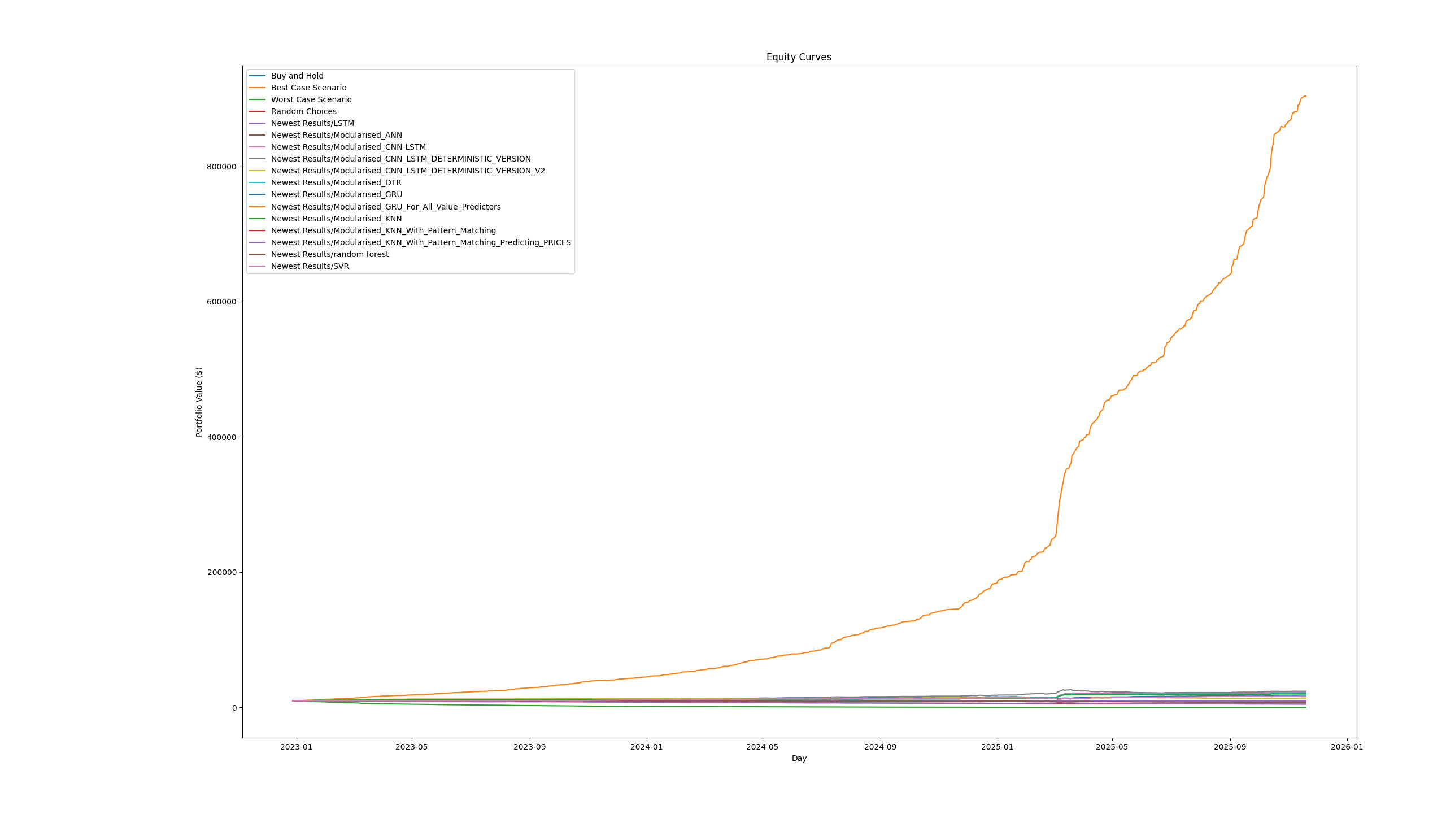

Backtesting Results

Best Model Performance

*Equity curve showing the best theoretical possible performance for a comparison.

*Equity curve showing the best theoretical possible performance for a comparison.

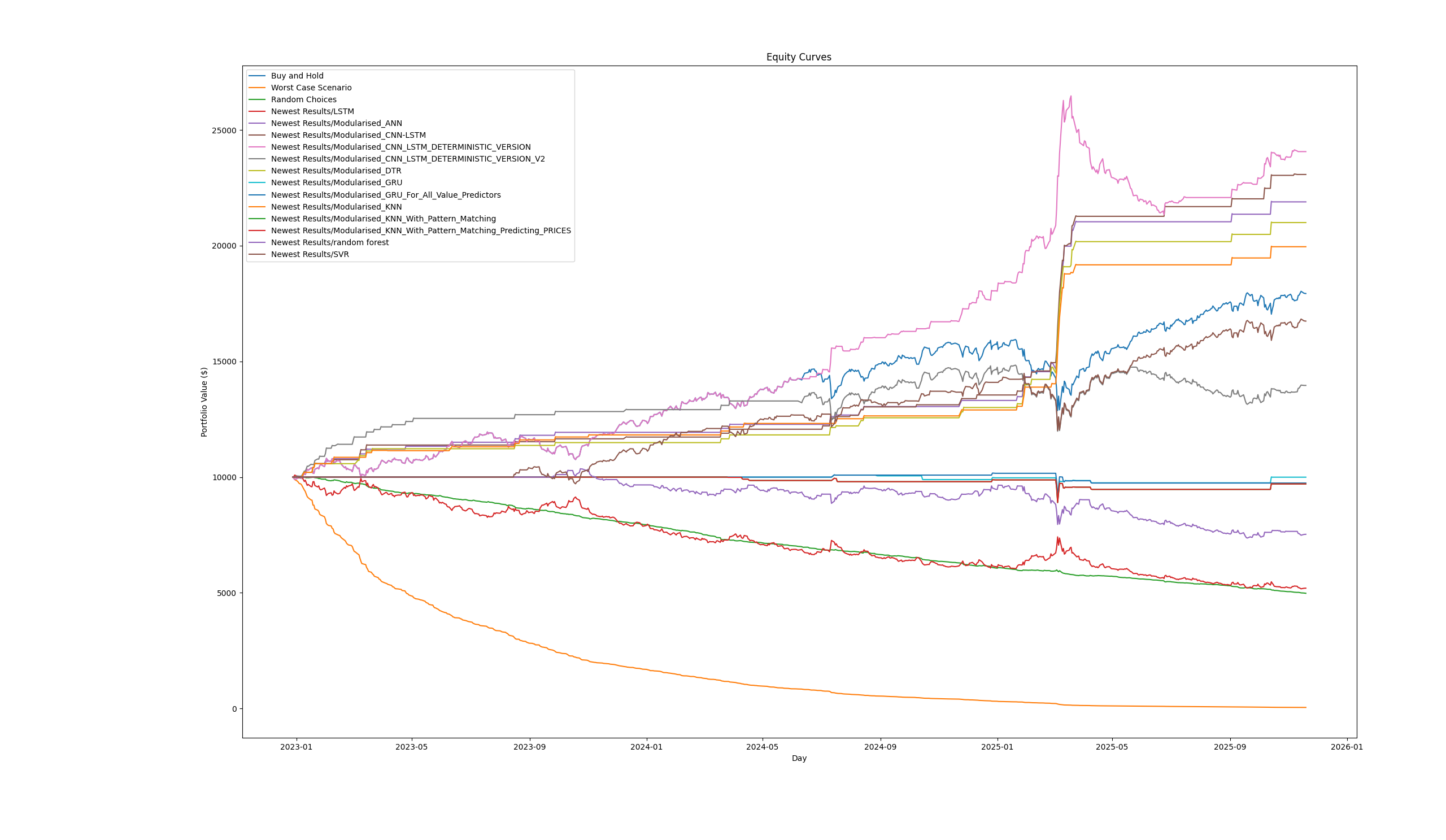

Without the Best Theoretical

Key Insight: Accuracy ≠ Profit

The most important finding: DTR achieved RMSE 3.42 (99.5% accuracy in price prediction) but only 59.5% directional accuracy — and that 59.5% directional accuracy is what actually matters for trading.

This demonstrates the gap between prediction accuracy and profitable trading:

- Predicting close prices to within $3 is impressive

- But getting the direction right only 59% of the time gives a slim edge over 50% random guessing

- The backtesting strategy exploits this slim edge consistently, resulting in 200%+ returns over the test period

Group Contributions

Other Team Members Built:

- Random Forest regressor

- LSTM implementation (group version)

- Linear Regression baseline

- Support Vector Regressor (SVR)

- Website and results presentation

Repository Structure:

- Personal repo — My individual model implementations and backtesting engine

- Group repo — Integrated models, database schema, and final results

- Website repo — Frontend for displaying hindcast and forward predictions

Database & Data Pipeline

Architecture:

- 30+ years of historical OHLCV data sourced via

yfinance - MySQL backend for efficient storage and retrieval

- Normalisation testing (1NF → 6NF) to optimise query performance

- Data pipeline for daily updates and feature engineering

Dataset Size: ~800 MiB raw; heavily indexed for ML training

Methodology

Prediction Pipeline

- Feature Engineering — Technical indicators (MA, RSI, MACD), lag features, volatility measures

- Train/Test Split — 25 years training data, 5 years held-out test period

- Prediction Task — Weekly ahead forecasts for OHLC prices

- Backtesting — Simulate trading strategies based on model predictions

- Walk-Forward Validation — Retrain models periodically to avoid look-ahead bias

Backtesting Strategy

The custom backtesting engine:

- Evaluated each model’s predictions against actual price movements

- Simulated trades based on directional confidence (buy when predicted > current, sell when predicted < current)

- Incorporated realistic assumptions: commissions, slippage, market hours

- Tracked equity curve, Sharpe ratio, maximum drawdown, and win rate

Key Findings

- DTR vastly outperformed neural and classical approaches in prediction accuracy (RMSE 3.42 vs 30+)

- Pattern matching (KNN-PM) achieved surprising directional accuracy (71.9%) despite higher RMSE

- High prediction accuracy does not guarantee high trading profit — directional accuracy, not absolute error, is the limiting factor

- Ensemble approaches combining multiple models improved robustness and reduced overfitting

- A 9% edge in directional accuracy (59% vs 50%) compounds to 200%+ returns over multi-year backtests

Tech Stack

Python · PyTorch · scikit-learn · Pandas · NumPy · yfinance · MySQL · Matplotlib

COMP208 Group Project; demonstrates end-to-end ML pipeline from data acquisition through deployment, with focus on trading applications and the realistic challenges of converting prediction accuracy into profitable strategies.